Stadium Financing

A primer on how stadium financing works.

As sport has entered an era of hyper-commercialization, with a relentless search for new revenue streams, one critical revenue pillar has emerged – new stadiums. By now you have probably seen hundreds of posts and discussions on this topic, so I will skip pontificating too much about stadiums as commercial engines for the sports teams.

Instead, this is a primer on how building of the stadiums is actually financed.

Stadium financing

Today, stadiums are among the most complex and expensive real estate assets. These projects can cost billions of dollars, and no single party – team owners, local governments, or private investors shoulder the entire burden alone.

The financing involves a mix of debt instruments, public subsidies, private equity, and increasingly creative financial engineering.

At its core, stadium financing is a bet that the venue will generate predictable, long-term revenues to repay lenders and investors.

Why new stadiums

For two decades broadcasting revenue has been the biggest driver of revenue growth. Today it is plateauing and getting concentrated in a fewer properties. That leaves clubs searching for new, controllable revenue streams, New or upgraded stadiums have emerged as the answer.

In 2025 Deloitte estimated over 300 sports stadiums globally have begun renovations or new builds. And looking at the top 20 football clubs in Deloitte’s 2026 Football Money League, the fastest-growing revenue segment is matchday income.

Modern stadiums and mixed-use districts are transforming sports venues into 365-day entertainment destinations, unlocking multiple new revenue streams:

Premium seating: VIP boxes, suites as a hospitality product

Sophisticated food & beverage

New naming rights: a critical component

Non-matchday events: concerts, conferences and festivals

From financing perspective, multiple revenue streams stabilize and diversify cash flows, reducing lenders risk.

Types of stadium financing

Stadium financing generally falls into three broad categories:

Loans (banks and private credit)

Public bond issuance (US local authorities)

Rated private placements

Different financing instruments play a distinct role in the lifecycle of a stadium project, and reflect corresponding risk. Risk is very different during construction, and once the stadium is open and generating predictable cash flows. Specific instruments can also monetise particular revenue streams.

Bank loans and private credit

Detail: A senior secured construction loan is often the first debt solution. An initial credit facility gives the owner the speed and certainty to go ahead with construction before more complex longer-term capital markets financing can be arranged. These loans can fund construction-phase risk when stadiums do not generate revenue.

Structure: Stadium construction is complex and expensive, and can be unpredictable. The borrower needs capital over time, so these credit facilities are not fully drawn upfront. They have flexible drawdowns and the ability to adjust to changing project needs. The borrower may need to demonstrate they have completed certain milestones before making new drawdowns.

Depending on the size of facility there can be a single lender or a club of lenders.

Interest: Floating rate

Very dependent on the situation, usually 7% to 12%, but it can also be higher.

Fulham secured a 5-year loan facility for the development of the new Riverside Stand with interest charged at the SONIA plus 3.625% (currently ~7.7%)

Rating: Not required, and almost never rated

Guarantees: Given the construction risk, at this stage lenders may require some level of guarantees from the owners because stadium does not yet have revenues.

Terms: Loans tend to be for 3 to 7 years, with floating interest rates.

Lenders: While traditional banks are still playing a key part, since the GFC construction loans have become particularly challenging for banks from the perspective of regulatory capital requirements under the Basel III framework, requiring banks to hold more capital against potential losses. Now private credit has stepped into this gap.

JPMorgan is unequivocal leader in the space, having financed 65% of major stadium developments in the US and Europe (Everton and Fulham in EPL). Goldman Sachs also has specialized sports financing practice.

Large private credit providers like Apollo and Ares are looking to deploy significant amounts of capital for stadium financing.

Municipal public bonds (US)

Detail: Bonds play a major role in stadium financing, especially in the US, where large part of funding is coming from the local governments. Public bonds are generally used for large-scale stadium projects where public entities (e.g. municipalities) are financing the construction through tax revenue sources.

In the US public funding for stadiums typically funds the surrounding infrastructure needed for these large-scale projects, like roads, public transit, and utilities. For example, Chicago Bears’ proposed stadium project has a comprehensive infrastructure plan estimated to cost $1.5 billion out of ~$5 billion total cost.

Structure: Municipalities can issue general obligation bonds backed by the taxing power of the issuing government; or revenue bonds, which tie principal and interest payments to specific income streams generated by the facility, often from a dedicated tax.

Interest: Fixed

Municipal stadium bond coupon rates generally fall within the 3.5% to 5.5% range.

Rating: Required

Rating will depend on the issuer. Many US municipalities and cities have high investment grade ratings, often in the AA to AAA range.

Tax-exemption: Municipal bonds are typically tax-exempt – their interest is exempt from federal and state/local income taxes, resulting in lower interest rates, which is lowering the cost of borrowing for local governments and total cost of stadiums.

Certain public purpose thresholds must be met to qualify for tax-exemption. Specifically, no more than 10% of proceeds can be used for stadium, and most funding has to be used to fund surrounding infrastructure.

Terms: 15 – 30 year maturities, matching the lifespan of the facility.

Semi-annual interest payments.

Call Provisions – Municipalities often use optional or mandatory calls, allowing them to pay off the debt early if refinancing opportunities arise

Investors/Lenders: Public bonds with wide investor base, including fans of the clubs.

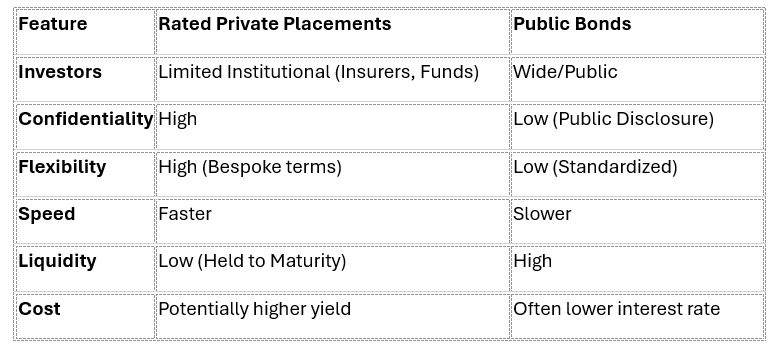

Rated private placement debt

Detail: A private placement is a privately marketed, long-term corporate debt offering (note / bond). They are increasingly used to refinance construction loans once the stadium is operational and revenue streams are established. They are also often used to fund stadium upgrades.

PPs are often suited for smaller or riskier borrowers requiring flexibility, while public bonds are often secured by stable public tax revenues.

Structure: Unlike loans, the maturity of private placements notes can extend 20 to 30 years, with fixed rates that give clubs certainty on servicing costs.

The debt is structured to satisfy project finance rating criteria and to achieve a higher credit rating than the underlying team might warrant on a standalone basis, leading to lower cost of borrowing.

Interest: Fixed

Typically offers fixed-rate coupons of 6% to 9%.

Sporting Lisbon raised €225 million in 2025 through a 28-year bond (BBB-) with a fixed annual interest rate of 5.75%.

FC Barcelona has refinanced €424 million stadium debt in 2025 with new bonds at an average interest rate of 5.19%.

This was of course lower during the ZIRP. For instance, Tottenham sold £525m of US private placements in 2019 with coupons between 2.6% and 2.9%.

Rating: Not required, but they are almost always rated

They will usually have a low investment grade rating, or one or two notches below investment grade.

Securitization: Recently some clubs have started to securitize stadium debt into tranches with varying levels of risk and return to appeal to wider group of investors. Recently, Valencia and FC Barcelona applied this approach.

Terms: 20 – 30 year maturities, that matches the long-term revenue streams of stadiums.

Investors/Lenders: Marketed to smaller group of qualified institutional investors (pension fund, insurances, corporates)

Key Comparison Table

Security and Collateral

Stadium financing has some similarity with traditional project finance, but it also has some unique characteristics.

Non-recourse financing: The debt is issued by a newly formed SPV (“StadCo”), with assets and cash flows ring-fenced from the operating risks of the team (“TeamCo”). This protects the clubs from financial failure in case of defult.

Security package: Typically include a pledge over the stadium asset itself, assignment of key revenue contracts (naming rights, sponsorship agreements, broadcast-related income), and often a mortgage or charge over the land. If the borrower defaults, secured creditors have a legal right to the collateral.

Flow-of-funds: StadCo will lease the stadium to TeamCo and collect revenues generated by TeamCo. Revenue accounts are structured through controlled waterfall that prioritizes debt service, reserves, and maintenance before any excess flows to the team.

Credit risk

Credit risk in stadium finance is nuanced, and changes throughout the lifecycle of the stadium.

Construction risk is significant and cost overruns are common. The cost to build most modern professional sports stadiums has skyrocketed over the last decade, often into the billion-dollar range. For example, the new Buffalo Bills stadium saw its budget swell beyond $2.1 billion, driven by a $560 million overrun.

Once stadiums are opened financing structure is designed to achieve an investment-grade rating that is often higher than the team’s standalone credit profile. However, revenue still depends on team performance, fan attendance, specific league and the broader sport and entertainment market.

Ultimately stadiums are single-purpose sports facilities with limited alternative use value.

Europe vs. the US

The US and European financing models diverge significantly. American stadium finance is characterized by heavy municipal involvement, tax-exempt bond markets, and a tradition of public subsidy; although the trend is shifting toward hybrid public-private structures.

Since 2000, the US state and local governments have committed $19 billion, or about $330 million per facility, to fund new major league professional sports venues.

European clubs have historically financed stadiums through commercial lending, private placements, and increasingly, securitization. The concept of taxpayer-funded stadiums is far less culturally and politically accepted in Europe.

However, European clubs are now adopting the American playbook of stadium-anchored entertainment districts, and US banks are private credit lenders are increasingly active in Europe.

Final word

Stadium financing sits at the intersection of sports, real estate, public policy, and capital markets. As more projects advance over the coming years, the largest-ticket private credit opportunities in sport will be in stadium financing.

Thanks for reading,

Nikola

Awesome read, great blend of finance and sports. I’ve worked in securitisation, so it was especially interesting to connect my experience in that space with my passion for sports.

Do you think securitisation is becoming more of a trend here?

It feels well-suited to the model with multiple stable cash flows (like media and naming rights, plus season ticket revenue) that can be structured into waterfalls for investors to analyse.

Curious to hear your thoughts.

I’d love to be able to nerd out and see some of the debt structures behind these stadiums 🤓

Nik you are the gift that keeps on giving. Thank you for sharing your knowledge. Can I send a dm